China’s Chokehold On Rare-Earth Minerals Raises Concerns

China’s Chokehold On Rare-Earth Minerals Raises Concerns

SINGAPORE: In the race to build superior industrial and military products, China has a key advantage: the world’s biggest reserves of rare-earth minerals that are essential to producing some of the newest technologies. Western businesses have been increasingly concerned by this domination, and China’s recent informal stoppage of exports of rare- earth material to Japan pushed the issue to the front burner.

China dominates mining of rare earths used in an increasingly wide array of civilian and defense applications. Rare earths are essential for hundreds of commercial as well as military applications: electric motors and batteries for hybrid cars, wind-power turbines and solar panels, mobile phones, cameras, portable x-ray units, energy-efficient light bulbs and stadium lights, fiber optics, glass additives and polishing In a technology-intensive world, these rare earths have become some of the most sought-after materials in modern manufacturing, even though they’re used in relatively small amounts.

The late paramount leader of China, Deng Xiaoping, once said that rare earths would be to China what oil was to the Middle East. Now policymakers and corporate leaders in the United States, Japan, Europe and other advanced economies watch with mounting concern as China exerts market dominance by restricting exports and driving prices higher.

This concern was heightened when Japan, the world’s biggest importer of rare earths, reported last month that China had temporarily blocked shipments for political reasons, after Tokyo detained a Chinese trawler captain in a bitter dispute between Asia’s two top economies over the ownership of islands and valuable fisheries and seabed energy resources in the East China Sea.

|

Interactive Map: Rare Earth Mineral Locations Across the Globe

|

However, Beijing may have overplayed its hand. China’s moves have sent major consuming countries scurrying to secure sources of supply outside China: building stockpiles, providing incentives for domestic firms to mine and process rare earths, and finding alternative ways of make high-tech products that reduce reliance on rare earths.

The US Geological Survey says that substitutes are available for many applications, but generally are less effective. Still, Japan announced earlier this month that it had developed the first high-performance motor, free of rare earths, for petrol-electric hybrid vehicles.

The House of Representatives in Washington recently approved legislation to support revival of the once leading-edge rare-earths industry in the US, while the Energy Department says it will release a plan this autumn for developing more rare-earth metal supplies, in part by encouraging US trading partners to hasten expansion of production.

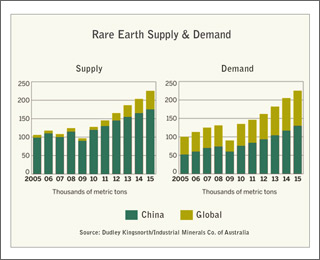

Yet China could keep its dominant grip on the rare-earths industry for some years. It holds 35 percent of global reserves, but supplies over 95 percent of demand for rare-earth oxides, of which 60 percent is domestic, according to Industrial Minerals Company of Australia, a consultancy. Just as important, Chinese companies, many of them state-controlled, have advanced in their quest to make China the world leader in processing rare-earth metals into finished materials.

Success in this quest could give China a decisive advantage not just in civilian industry, including clean energy, but also in military production if Chinese manufacturers were given preferential treatment over foreign competitors.

Cerium is the most abundant of the 17 rare earths, all of which have similar chemical properties. A cerium-based coating is non-corrosive and has significant military applications. The Pentagon is due to finish a report soon on the risks of US military dependence on rare earths from China. Their use is widespread in the defense systems of the US, its allies, and other countries that buy its weapons and equipment.

In a report to the US Congress in April, the Government Accountability Office said that it had been told by officials and defense industry executives that where rare-earth alloys and other materials were used in military systems, they were “responsible for the functionality of the component and would be difficult to replace without losing performance.”

For example, fin actuators in precision-guided bombs are specifically designed around the capabilities of neodymium iron boron rare-earth magnets. The main US battle tank, the M1A2 Abrams, has a reference and navigation system that relies on samarium cobalt magnets from China. An official report last year on the US national defense stockpile said that shortages of four rare earths – lanthanum, cerium, europium and gadolinium – had already caused delays in producing some weapons. It recommended further study to determine the severity of the delays.

China recently cut its rare-earth export quotas by 72 per cent for the second half of this year. According to one industry estimate, worldwide rare-earth demand is expected to exceed supply by as much as 50,000 tons by 2012 unless major new production sources are developed.

Chinese officials say that mass extraction of rare earths is causing extensive environmental damage in China and that’s why the government has tightened controls over exploration, production and trade. Poisonous chemicals are used to mine rare earths, putting local water supplies and public health at risk.

Meanwhile, the US appears to be the victim of its own astonishing lack of foresight in security-related industrial policy. Until around 1990, the US was self-sufficient in rare earths and the world leader in processing and use. Yet within a decade, the US became more than 90 percent reliant on rare earths imported either directly from China or from countries that received plant-feed materials from China.

Environmental and regulatory problems made mining and processing unattractive at the rare-earth site at Mountain Pass in California, which closed in 2002. Meanwhile, lower costs in China, continued expansion of electronics and other manufacturing in Asia based on rare earths, and the size and concentration of Chinese rare-earth deposits drove the shift in comparative advantage from the US to China.

Although tagged “rare,” rare earths are relatively common and widely dispersed around the world. However, in contrast to ordinary base and precious metals, they’re seldom found concentrated in exploitable ore deposits.

Of the nearly 100 million tons of known global reserves that can be economically extracted, 36,000 tons are at opposite ends of China, in the south and up north in Inner Mongolia. Russia and other states of the former Soviet Union have 19 million tons of reserves; the US, 13 million tons; Australia, 5.4 million tons; and India, 3.1 million tons.

The surge in Chinese rare-earth output initially flooded the market, cutting prices and stimulating new applications. Now with China seeking to capitalize on its advantage, the US and other advanced economies are trying to rush alternative rare-earth mines into production to reduce reliance on China and improve security of supply.

While demand is forecast to increase by around two thirds over the next five years, the US Geological Survey says that undiscovered resources are thought to be very large relative to expected demand. However, bringing new mines into production will take several years. And although the GAO report said that rare-earth deposits in the US, Canada, Australia and South Africa could be mined by 2014, rebuilding the US rare-earth supply chain might take up to 15 years. Meanwhile, China will hold sway and serve a cautionary note on global interdependence and reliance of high technology.