Dealing with a Declining Dollar – Part II

Dealing with a Declining Dollar – Part II

MEDFORD: US President George W. Bush's US$2.57 trillion budget proposal has brought a tepid domestic reaction, and foreigners seeking a silver-lining have little reason to rejoice either. From politicians to Wall Street economists, critics remain doubtful that the Bush budget offers a realistic plan for deficit reduction needed for a stable world economy. The plan, which calls for across-the-board restrictions on domestic spending, requires Congressional approval – unlikely, especially considering the previous rejection of many proposed cuts. Realistically, only about 30 percent of spending cuts are feasible, an inadequate amount for substantial deficit reduction.

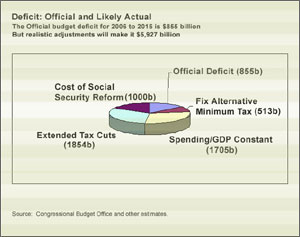

More so than this year's deficits, the ten-year projections may truly raise eyebrows: Over the next decade, the United States may accrue several trillion dollars in debt. Should that be the case, the dollar will likely be in danger; a worldwide "run on the dollar" would bear incalculable consequences.

All major nations have problematic long-term public finances due to their aging populations and overly generous promises of pensions and medical care for the elderly. However, among these nations, only the United States requires international borrowing to finance its public deficits. The large and growing current account deficit – the shortfall between the country's export and import – could trigger a sharp fall in the dollar, bringing in its wake rising interest rates and a recession, or worse. US trading partners could not be sheltered from the fallout.

The prospect of continuing budget and trade deficits poses a problem for potential foreign buyers of dollar assets. There is little doubt that the US economy has a faster long-run growth potential than Europe or Japan. Its financial markets are larger and more liquid. Its rate of return to capital is normally higher, and its accounting is no worse – arguably better – in spite of Enron-type scandals. The long-run public finances of the EU and Japan are in comparatively worse shape due to lower birth rates and more limited immigration, as well as more generous promised benefits. These are all good reasons to accumulate dollar-denominated assets, especially when the euro or yen buys more dollars than before.

On the other hand, the US consumers are mired in debt: Disposable income increased US$2 trillion from 1999 to 2004, while mortgages and other consumer debt increased nearly twice as much. Consumers, therefore, will likely be hit should home prices decline or interest rates increase. There is a real risk in buying dollar assets, even though the US government (unlike most other debtors) can print dollars to repay what it has borrowed. The large tax cuts have removed room for further stimulus. The Federal Reserve might lose control of interest rates if foreign buyers of government bonds stopped buying. Even Alan Greenspan and other Fed officials have expressed concern about the current and projected levels of current account deficits. If others began to sell dollars, there is little doubt that a "run for the exits" could develop, pulling the value of the dollar sharply down.

Buyers might assume that central banks would not allow a large dollar decline, since it would hurt the world economy. They would buy dollar assets, expecting that governments would safeguard their bets. This is called moral hazard, and it can make eventual adjustments even worse, as debtor nations found out in the Asian crisis. Even if central banks do prevent the dollar's collapse, a large hedge fund or other investor might still place its currency bets on a losing scenario. Ultimately, this would disrupt financial markets, as nearly happened with Long Term Capital Management, the hedge fund that collapsed a few years ago.

Were there clear indications that reducing the US federal deficit were a priority, the chance and severity of negative outcomes would decrease considerably. However, while a minority of Republicans and some Democrats remain "deficit hawks," a powerful group still maintains, as does Vice-President Cheney, that "deficits don't matter." This group prioritizes extended tax cuts and social security reform over deficit reduction. Without a reduction in spending on Iraq and entitlement (especially Medicare) reform and controls on other types of spending, it will be very hard to make a substantial dent in the deficit.

If US domestic politics make serious deficit reduction unlikely, the uneasy international bond buyers may ultimately force the administration's hand. If the Republicans wish to avoid wearing a "Herbert Hoover necklace" (President Hoover's policies brought about the crash of 1929.) around their necks for a generation, they may decide that preventing a dollar collapse is even more important than expanding spending and extending tax cuts. Or they might gamble that others have more to lose, and continue to run both federal and current account deficits that push the limits of foreign asset buyers' acceptance. The willingness of foreign central banks to accumulate dollar assets for mercantilist purposes makes this bet seem safer in the short term, but also makes it riskier over time. The whole world has a stake in the outcome of this debate, but few can vote – except with their money. Investors might cast the deciding votes; though if it comes to that, there could be more losers than winners.

For those who wish to glimpse the "tipping point" – if indeed there is one – the pace of Federal Reserve short-term interest rate hikes might provide a clue. If foreigners begin to sell Treasury bills, which still yield little more than inflation, the Fed would have little choice but to raise interest rates more quickly than it has indicated. These increases would transmit themselves to longer-term interest rates as well, and would drive up mortgage and other borrowing costs. Corporate investment, construction, and durable goods purchases (cars, furniture) would all diminish. Exports would benefit, but the net impact would be negative. If the rate hikes were steep enough, a recession would likely ensue.

Foreign central bankers would understand the fragility of their own economies and would want to keep exporting to the US market. This would tend to push them to purchase more dollar debt. However, fear of private selling of dollar debt or of a "rogue" central bank getting out of dollar assets early might create a sense of caution. With the US current account deficit over US$700 billion this year, even a slowdown in buying of debt would push the dollar down and interest rates up. This has not happened yet, but without corrective action the risks are clearly increasing. Will Washington take heed or not?

David Dapice is Associate Professor of Economics at Tufts University and the economist of the Vietnam Program at Harvard University’s Kennedy School of Government.