Denying Imbalances, G20 Risks Chaos – Part III

Denying Imbalances, G20 Risks Chaos – Part III

BEIJING: The failure of the G20 and the eurozone to resolve their problems, highlighted by the abortive summit in Cannes, throws into sharp relief the flip side of globalization. The seemingly inexorable increase in the flow of goods and finance ’round the planet that marked the first decade of this century has been replaced by the ever-rising risk of contraction. That risk is all the greater precisely because of the way global interconnections have flourished, especially since China joined the World Trade Organization at the end of 2001, and the current inability of government leaders to handle adversity.

The flop in Cannes is the latest of a string of summits that have fallen short of what they should have achieved. But its timing and the reasons for failure give it a particular resonance which is likely to affect both global relations and domestic politics and policymaking from Beijing to Berlin via Washington.

The economic and financial crisis is serious enough, but underlying it is a deeper issue of confidence in political leadership. If Barack Obama, Hu Jintao and the leaders of Europe cannot come up with at least the start of a common response to the gathering global downturn, where is the world to look for salvation? If the eurozone is still floundering to come to grips with crisis 18 months after Greece received its first bailout package, what belief can anybody have in the ability of the common currency’s institutions and managers?

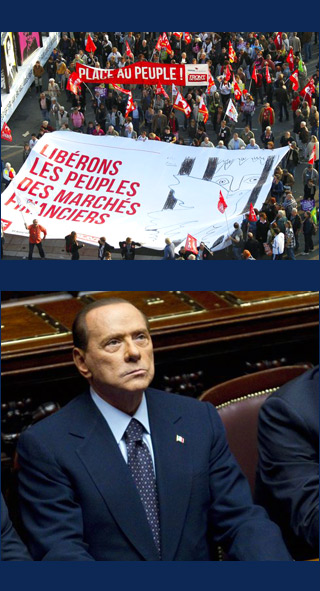

Global leadership has been found sadly wanting as it seeks refuge in grand statements that carry all the credibility of a fairground barker. The arms-length stance of the Obama administration, its refusal to put a figure on the increase in the resources for the International Monetary Fund, has shown more clearly than anything how Washington is unwilling and incapable of playing the international role it has assumed since 1945. Eurozone chieftains have managed to make fools of themselves, and very publicly into the bargain. Within a week of President Nicolas Sarkozy and Chancellor Angela Merkel announcing that they had reached an “ambitious, credible and durable” solution to the crisis that began in Greece, matters only got worse with the pantomime of Greece’s on-off referendum and a deepening morass in Italy, leading to the planned resignation of Prime Minister Silvio Berlusconi, pending approval of budget reforms.

Who can be surprised if markets make hay from such confusion and lack of purpose as risk premiums soar, interbank lending freezes up together with the trade finance essential to international commerce? Who can but note the seemingly inevitable death of the Doha Round of trade talks, meant to move the world to a new level of free exchanges? Who can fail to mark the way in which China continues to insist that domestic growth is its first priority? As for the one apparently positive outcome in agreement on the flexibility of exchange rates, China’s reserves have continued to grow since it adopted a flexible basket for the yuan in June 2010 – and Beijing has pointed out that flexibility means a currency may go down as well as up.

Instead of new ideas to promote global growth, reduce imbalances and instill confidence – concrete measures with concrete results – governments are cloaking themselves with grandiose pronouncements about the future and imposing austerity. The two make a bad fit. Expressions of confidence by European leaders ring hollow as the reality, what matters to their populations, is that their countries probably won't show any growth as a group, with Mario Draghi, the new president of the European Central Bank, talking of a mild recession. French Prime Minister François Fillon announced during the weekend that his government would pursue the “most rigorous” policies seen for 65 years. So far “austerity” is a merely a word for most Europeans with their $2 trillion debt pile; as it bites in the coming year, the awakening will be harsh, with the mass protest reaction in the streets of Athens a likely harbinger.

The wider but unacknowledged sub-text to this is the threat posed to the opening up the world, reaching far beyond economics to span popular culture, travel, sport, communications, and most other spheres of life from food to fashion. Critics see this process which has taken wing in the past decade as a hypocritical mask for American-led capitalism, and the downsides are evident. Yet the benefits are tangible from Beijing to Barcelona. Leave aside the obvious beneficiaries in the rich world. In China more people have been made materially better off in a shorter space of time than ever before in human history. Earnings from trade enabled the Lula da Silva government to implement striking social programs. India’s GDP has more than trebled since 2000.

In what seemed like an inevitable process are interlocking gears that gave work to tens of millions of Chinese assembling iPhones in Shenzhen, thousands or Brazilian suppliers of iron ore and soy, which can seize up when the grease that politicians should provide is lacking. The danger is that, when faced with harsher times and more difficult decisions, governments fall back on their domestic concerns, which make a mockery of the G20’s ambitions to forge global solutions to global problems. With elections in both the US and France in 2012 and the wholesale leadership change in China next autumn and then the federal election in Germany in 2013, the temptations for politicians to focus on inward issues is strong.

This is likely to be accentuated by uncertainties over the prospects of incumbents and, in some countries, the rise of chauvinism. In Europe, far right-wing parties have wind on their sails. In France, the far-right National Front, which calls for withdrawal from the euro, is forecast to get more than 15 percent of the vote while last month’s Social Party primary to pick a challenger to Sarkozy gave 17 percent of the vote to anti-globalization candidate Arnaud Montebourg. Chinese blogs reflect growing nationalism while Beijing pitches far-reaching claims to sovereignty over the South China Sea and builds up its blue-water navy.

The shock that followed the collapse of Lehman Brothers three years ago was all the greater because so many people had assumed that the debt-fuelled gravy train would go on forever. In a similar way, the prevailing wisdom has been that the globalized world has established itself as the model for the 21st century. But its cogs could grind to a halt all too easily as the downward pressures ripple out from the developed world. If Europe goes into recession, for instance, Chinese growth risks dropping to the key 7 percent level needed to maintain an expansion on which the regime relies.

Beyond cold economic and financial reality, this is also a matter of politics and psychology. So far, the world’s leaders have failed to rise to the occasion. In the current mood of popular disenchantment with politicians, it is easy to brush away the G20 failure on the French Riviera as no more than par for the course. But the world faces a new, more testing set of challenges, which as much as Lehman Brothers, risk dragging it down on a broader front than it realizes.

Jonathan Fenby is author of the Penguin History of Modern China and will publish a study of contemporary China, Tiger Head, Snake Tails, in April 2012.