Global Crisis Spurs Long-Needed Change in China

Global Crisis Spurs Long-Needed Change in China

BEIJING: This is not the coming out party that China envisaged. Just as China emerges as the largest exporter in the world, the global market collapses and the world turns to China to offer a reprieve. China’s export machine is in a stall. Its stimulative measures will help, but may not be enough to generate the growth that the world and Chinese people have come to expect.

Each month’s data are most disheartening; January’s export figure showed an 18 percent decline from the year before. More alarming was the 43 percent drop in imports – many of those imports are parts and material for future processing, and their disappearance signals worse export performance in the months ahead. The government estimates that already 20 million migrant workers have lost jobs in manufacturing and construction. Painful as it is, the adjustment going on in China is necessary for the future healthy development of the economy. The trick is managing the adjustment so that it’s not too rapid or disruptive.

In recent years half of China’s output has gone to investment and net exports. Yet investment and net exports cannot be a source of growing demand forever. Trading partners, especially the US, cannot go on borrowing forever to cover consumption. The clever financial engineering disguised this for a while, but eventually the imbalances were exposed. As demand for imports from the US and other deficit countries dropped sharply, this reduced demand for China’s exports, with quick spillover effect on construction of both factories and residences. Growth of investment in the real estate sector dropped to zero in the last months of 2008. Steel production was down 20 percent from the year before; electricity use, down 10 percent. These are indicators that the old model of growth based on exports and investment hit a wall.

Alarmed at these declines, the government quickly put together a 4 trillion yuan stimulus package, worth US$586 billion, mostly of infrastructure projects. Some pundits immediately criticized this as an attempt to hang on to the old model, but those critiques are unfair. First, there have been few efforts to try to maintain exports, with the recognition that they do not make sense with current global conditions. Second, the infrastructure program contains a lot of projects aimed at strengthening consumption and quality of life: high-speed passenger rail, urban public transport, wastewater treatment and other environmental cleanup. However, all the details are not worked out yet, and there are some risks. In the Asian crisis of 1997-98, China stimulated its economy with a lot of infrastructure projects aimed at bottlenecks in roads, seaports, airports and power. Now, there are no major bottlenecks in those areas, yet some local governments would love new projects, even if they have little future payoff. So, the challenge is keeping the stimulus program focused on legitimate future needs, not white elephants.

Another concern about the stimulus package is that it aims at limiting the damage in the industrial sectors. Of course, the government wants to avoid allowing those sectors to decline too rapidly. But over time one would want relative decline of industry and a shift in the growth model. The other half of China’s GDP represents consumption. The half of the population that lives in rural areas consumes 9 percent of GDP; the urban half about three times more (26 percent). Government consumption – which includes the public spending on health and education – is only 13 percent. Both the welfare of Chinese people and sustainable long-term growth depend on increasing all those shares. The government has measures in all these areas: programs to subsidize appliance purchases by rural households; stimulus to the real estate sector, along with all the associated purchases of household items; 850 billion yuan over three years to spread health insurance to 90 percent of the population.

These programs all go in the right direction, and the issue is simply are they big enough to maintain a healthy rate of growth. Simple math shows that it will be hard to get growth out of consumption increases over one year. If rural real consumption grows 10 percent, which would be great in an overall contractionary environment, that adds 1 percentage point to GDP growth. An increase of 20 percent in government consumption adds 2.6 percentage points to growth.

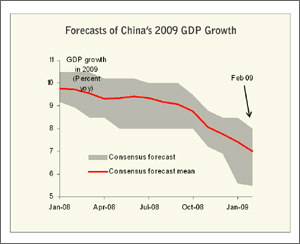

What all this adds up to is uncertainty about China’s growth rate in 2009. The consensus view is that the fourth quarter of 2008 and first quarter 2009 will be the bottom of the trough – though don’t be surprised if the first quarter growth rate is below last quarter’s 6.8 percent year-on-year change. The consensus forecast for 2009 is still 7 percent (see chart). Two caveats: There are a wide range of views, from 5.5 percent up to 8 percent; and, the consensus forecast for 2009 has been consistently marked down over the past year as new information, all bad, has become available.

Enlarge image

This leaves the question of how much China can contribute to global growth and stability. The first task is to limit the decline in China’s own growth. In academic circles there are some negative predictions that China’s growth could decline to 2 or 3 percent in 2009. That would be a shock to global confidence and a further blow to the commodity-exporting developing countries that send products to China. The negative view assumes that commercial investment will drop sharply in this environment, so that even with enhanced public investment in infrastructure, the net result for investment is zero growth. Yet China enters this crisis in excellent fiscal shape; hence it has huge potential to increase transfers through its minimum income support and other safety nets, build up health and education, and follow through on infrastructure projects. Hence, if growth continues to falter, my advice is, “think big” when it comes to government programs and spending this year.

A second key task for China is to keep open its trade regime and look for opportunities to liberalize further. China’s merchandise trade is quite open compared to other developing countries, and through its World Trade Organization commitments, the country has taken initial steps to open service markets. It would be a smart move to open these service markets further, including sectors like financial services, logistics, airlines, media, telecom and transport. In practice, this requires more openness to direct foreign investment.

While it’s a bold move to liberalize during a crisis, there are two good reasons for China to consider: First, global rebalancing will result in China’s trade surplus gradually declining. If service imports are rising rapidly, then the adjustment can go hand in hand with moderate expansion of manufacturing exports. If imports are not rising, however, then the adjustment may force a painful absolute decline in manufacturing. Second, more of China’s growth in the future will depend on service industries. In manufacturing China has used foreign trade and investment to create highly competitive markets with rapid productivity growth. However, services remain relatively backward and inefficient.

More openness and competition would create the same dynamism in services that China has already in manufacturing. Without that, the growing share of services in the economy could go together with a secular decline in overall growth.

The long-term health of both China’s economy and the global economic system largely depends on whether China successfully uses the crisis to make these needed adjustments.

David Dollar is World Bank country director for China and Mongolia, based in Beijing. For an ongoing discussion of economic, social and environmental issues, click here to read his blog.