Global Economy: Is Anybody in Control?

Global Economy: Is Anybody in Control?

MEDFORD: When European leaders interrupt their August vacations, they’ll return to their offices and learn just how bereft they are of ideas in dealing with the economic crisis threatening the world. From Washington to Brussels to Tokyo, leaders have been squabbling and fumbling, seemingly oblivious of the global threat. The farce in the Capitol Hill leading to the downgrading of US debt by Standard & Poor’s, the feckless response of the European Union to the spiraling sovereign debt crisis and the trade surplus prompting Japan’s devaluation of the yen all point to a dangerous bankruptcy in leadership.

In the US, bickering politicians drove the country to the brink of default, and their last-minute compromise failed in stopping the downgrading of US debt. Even before the downgrade, the economy was near stalling. Gains in jobs this year are less than half the amount needed to keep unemployment stable without more people dropping out of the labor force, as happened in July. Consumer confidence and spending, industrial output and leading indicators point toward a slow or no-growth scenario. Not only did the bitter dispute over deficit cutting and tax increases bring the country close to default, politicians even went home for recess leaving the country’s Federal Aviation Administration partially unfunded due to a dispute over $17 million in spending. The result was 70,000 unemployed and $30 million a day in lost tax revenues at a time when deficit reduction was declared to be job one.

US problems are serious but tractable if they could be discussed and resolved. There’s no indication that this will happen, additional proof that the recent downgrade and negative outlook by Standard & Poor’s was justified. Moody’s, another rating agency, kept the AAA rating, but posted a negative outlook.

The fact is that short-term fiscal restraint will make the current economic weakness more serious and reduce tax revenues, generating a weaker fiscal position over the next several years. Another round of monetary easing by the Federal Reserve is unlikely to accomplish much in the real economy and will increase the chance of speculative bubbles and inflationary potential. Interest rates the Fed controls are already near zero. Corporations hold $1500 billion in cash, but aren’t hiring. Housing, a sector that normally responds to low interest rates, is burdened by foreclosures. A lack of serious attention to Medicare and Medicaid will lead to deficits soaring in the medium term while productive and necessary discretionary spending is cut. Unless the opposing positions of “no cuts” and “no new taxes” are compromised, and this seems unlikely before 2013, the outlook for the US economy is grim.

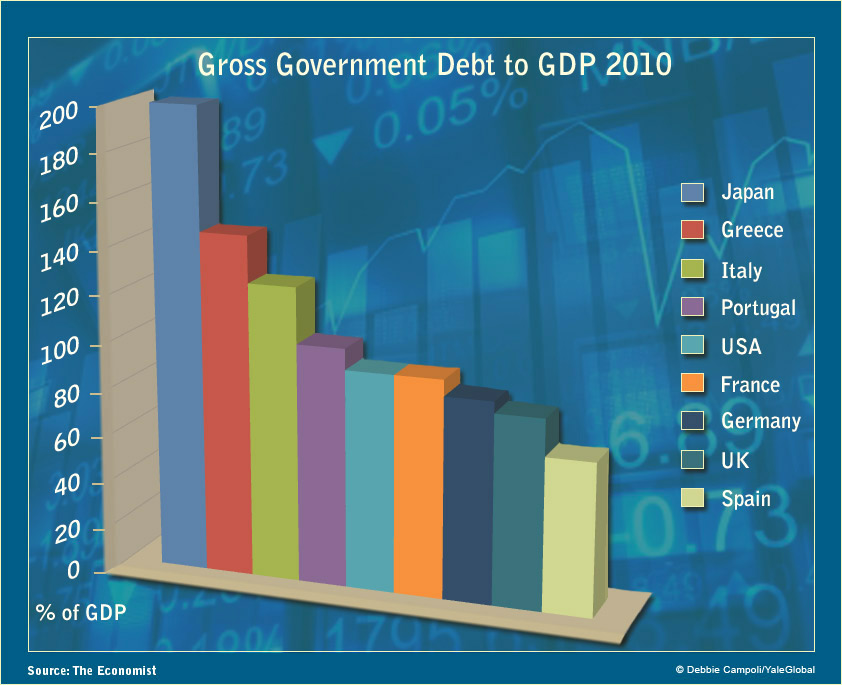

But it’s in Europe, not the US, that the crisis may turn into something truly awful. The European Central Bank just announced that it will reverse previous policy and buy long-term bonds of Italy and Spain. This amounts to a backdoor fiscal transfer, exposing the bank to future losses as was the case with the Greek bailout. European banks hold huge amounts of government debt from Italy, the world’s third largest official debt market, and Spain. Italy in particular, with a debt/GDP ratio of 120 percent and slow growth cannot afford for long to refinance its debt at 6 to 7 percent. If Italy had to reduce the principle or interest on its debt, many European banks would have their capital severely impaired, reducing lending and creating crisis in the euro zone.

It’s an open question if the European Central Bank can afford to replace private-sector purchases of Italian and Spanish debt. No doubt the bank hopes to reassure private investors of a lender of last resort.

A grudging and feckless response of European leaders to the crisis thus far has reduced rather than restored confidence. With upcoming elections in Spain and France, and with Italian political leadership weak at best, it will be difficult to take decisive action. Neither is it likely that Germany would allow a huge expansion of the money supply or a weakening of the European Central Bank balance sheet to buttress “Club Med” countries.

Europe faces a series of difficult choices from letting the euro collapse to subjecting a large fraction of its members to grinding contraction from extremely lax monetary policy. None of these are likely to be painless. All may have knock-out impact in the global economy.

In Japan, the debt to GDP ratio is an astonishing 200 percent, meaning its debt amounts to two years’ worth of wealth created by the country. With a shrinking population and huge costs associated with the tsunami recovery, it’s unclear how long the government can continue to run deficits of 8 to 9 percent of GDP a year. The usual trump cards – that most debt was bought by the Japanese and interest rates were low – may not hold for long. Still, the fact that the Japanese central bank is trying to weaken the yen to help exports at a time of a large trade surplus shows just how out of joint the economic situation is. If the elderly and insurance companies start to cash in their government bonds to finance retirement or payments for reconstruction, there may be increasing pressure on Japan to lower its deficits, increasing the chances of a recession. Output will fall this year due more to the supply-side impact of the tsunami and the reduced electricity supply.

One bright spot could be the emerging economies. They accounted for 38 percent of global GDP last year and many are growing rapidly. China is projected to grow 9 percent this year; India nearly 8 percent; Indonesia about 6 percent while Brazil and Russia are expected to slow to 4 percent. However, many are still directly or indirectly dependent on rich-country growth to sustain these rates. China managed to boost lending for questionable investments by local governments or their captive companies in 2008-09 and it’s not clear that they want to repeat this. Indonesia, Russia and Brazil rely on commodity exports to an uncomfortable degree, and many of these prices have begun to slide – oil has dropped 15 percent from recent highs. While these economies will continue to grow, they won’t offset additional weakness in demand from debt-heavy rich countries. Indeed, inflationary pressures in many of these countries have created some pressure for tighter monetary and fiscal policies, and this would add to a global slowdown.

The human cost of prolonged job drought will have a long-term impact. Young workers entering or wanting to enter the labor force, who fail to get a job or who get a poor job end up with lower earnings for decades afterwards. The long-term unemployed are less likely to get interviewed for good jobs and lose critical job skills. The absence of any serious discussion about these problems suggests they’ll go unsolved. Add to this the possibility of financial upheavals in bond and stock markets and reductions in wealth and financial stability of banks and older workers and the likelihood of longer term stagnation increasing. Perhaps the most disconcerting element in this is that few leaders or even intellectuals have ideas for solutions likely to be considered.

The world seems to be in a negative sum game where not letting the other side get its way is more important than avoiding large costs to one’s own group and all other players. Despite frequent talk of an interconnected world, the myopic leadership in the world’s leading countries seems oblivious to the fact that all are in one boat.

David Dapice is associate professor of economics at Tufts University and the economist of the Vietnam Program at Harvard University’s Kennedy School of Government.