The New Casinos – Emerging Markets

The New Casinos – Emerging Markets

TOKYO: Had William Shakespeare been an economist, he might have observed that some economies are born great, some achieve greatness while others have greatness thrust upon them. If alive today, he might include in the latter category so-called "emerging markets" many of which have in effect had fame, or at least familiarity, thrust upon them.

The result has been the creation a widespread belief that "emerging" markets or economies are approaching developed country status whereas, in fact, their physical, institutional and financial infrastructures remain relatively weak. Their stock markets have become casinos where chips are bought and sold largely by foreign investors, with marginal benefit to the domestic economy.

A couple of decades or so ago, relatively few people had heard of emerging markets, and far fewer of "frontier" markets. Yet today these territories are constantly in the news, the subject of regular claims about being poised, if not exactly to take over the world then, at least, to account for the lion's share of global GDP within a decade or so.

That the progress of many among this group of 50 to 70 emerging markets, depending upon definition, has been impressive is undeniable. But as a group they have achieved a prominence that belies the relative lack of economic, financial, political, social and institutional development they still need to overcome before they can truly be said to have "emerged."

The fact that a highly diverse group of economies have been labelled as "markets" is revealing as to why they have achieved prominence in a relatively short space of time. They have been "packaged" by Wall Street investment bankers and sold to international fund managers anxious to acquire overseas assets in line with the ongoing process of globalization.

This has been one of history's greatest exercises in marketing, and the result has been that a bunch of countries which not so very long ago were of interest mainly to development professionals – economists, engineers or social specialists – which were known as "developing" or "third world" economies, "basket cases" even in some instances, are now regarded as vibrant and dynamic emerging economies.

Some might argue that this has been all to the good, raising the self-esteem of countries concerned while also boosting their image among the international community. But globalization of portfolio investment has also tended to create an assumption that by connecting developing countries to flows of international investment, development challenges can be overcome.

This is often not the case, however, as glaring deficiencies of development come to light even after emerging markets supposedly graduated to a new “emerged” status. Among these deficiencies is their relative lack of basic infrastructure such as highways, railroads, power grids and sanitation networks, not to mention health and education systems.

The projected cost of such infrastructure – $8 trillion in Asia alone over the current decade, as estimated by the Asian Development Bank, and $57 trillion globally as estimated by the Organization of Economic and Co-operative Development – vastly outstrips the $1 trillion or so of private capital that flows annually from advanced to emerging economies, as estimated by the Institute of International Finance.

These discrepancies between supply and demand only begin to hint at the true scale and nature of the problem, however, which is that the packaging of emerging economies in a way that makes them attractive to global portfolio investors encourages an often short-term and superficial or "cherry picking" approach to financing their economic development.

Foreign portfolio capital, that is investment into stocks and bonds, naturally seeks the highest return in the shortest possible period of time and prefers existing enterprise with a track record of profit-making rather than so called "greenfield" ventures in projects such as infrastructure with a long gestation and payoff period.

Likewise foreign "direct investment," where corporate capital is directed into new ventures, tends to prefer manufacturing or service enterprises that produce returns in a few years rather than longer-term projects such as infrastructure. The upshot is that emerging economies receive an inadequate and unbalanced diet of funding.

Not only that, but the need for development of domestic financial systems that are vital to national economic wellbeing in emerging economies is often overlooked by those who focus on the supposed need to bring developing economies into the global marketplace for capital. Put bluntly, it is a case of emerging markets being exploited by the market itself.

This raises the question of how and why emerging markets did in fact "go to market." Very simply, it’s “because savings in Europe began to exceed local demand [for investment] in Europe" during the late 1970s and in the 1980s, in the words of David Gill who might fairly be called the "father" of emerging markets.

This led to a desire on the part of European and later US investors to acquire portfolio assets outside of their own borders, according to Gill, who was managing director of the capital markets department at the World Bank's International Finance Corporation, IFC, during the seminal years of emerging-market development.

It was principally pressure applied from advanced economies, or rather from agencies acting on behalf of the Western investment community, rather than internal motivation that precipitated the activation of stock markets across the developing world, beyond the relative few that had had such markets for decades as part of a colonial legacy.

Antoine van Agtmael, a former investment banker at Bankers Trust in New York who later joined IFC, recalls that in 1981 when he "pitched the idea of a third world equity fund" to Salomon Brothers, he was told that it would never sell under that name. So, he came up with the label "emerging markets" – which stuck.

The marketing of these economies has been a remarkable success. Today, the value of stocks listed on the world's emerging markets is around one quarter of the global value or capitalization of all listed stocks and that should reach one half within the next 20 years, according to estimates by Goldman Sachs.

Among the most prominent of the emerging markets are China, Brazil, Russia, India, Mexico, Turkey, South Africa, South Korea and Taiwan while so-called "frontier" or not-yet-emerging markets include countries such as Argentina, Ukraine, Romania, Bulgaria, Kazakhstan, Lebanon, Jordan, Vietnam and others in various parts of Africa.

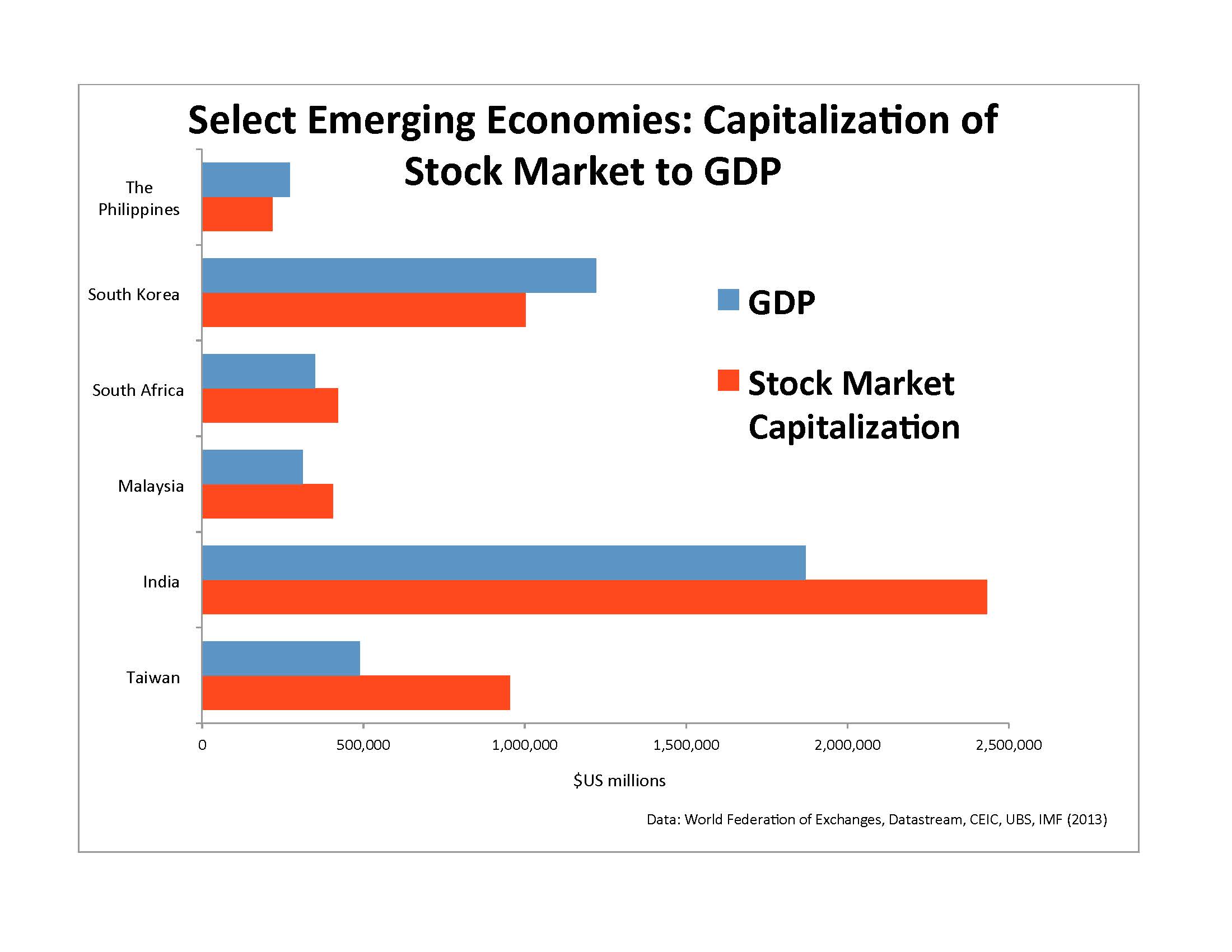

The aggregate value of emerging market stocks exceeds that of those quoted on the New York Stock Exchange, and in some of these markets the total stock market value or "capitalization" of listed stocks exceeds the size of the country's economy. This reveals the huge discrepancy between stock values driven by foreign funds and the actual capital-raising ability of local stock exchanges for the domestic economy. In this sense, they are casinos.

Stock markets do play an essential role within any financial system, but the equity market mania that has driven their development in many emerging economies has arguably been at the expense of the development of banking systems and bond markets essential for raising long term funds and of investment institutions capable of channeling local savings into local investment.

This says nothing, moreover, of the problems caused by the introduction of extremely volatile foreign capital flows into emerging economies via their stock markets, causing the creation, and subsequent destruction, of asset bubbles and posing problems for the conduct of domestic monetary policy. All of which suggests that stock markets have "emerged" prematurely across much of the developing world.

Anthony Rowley is a former business editor and international finance editor of the Far Eastern Economic Review and is currently field editor (Japan) for Oxford Analytica and Tokyo correspondent of the Singapore Business Times. During a long career in journalism, Rowley has written extensively on issues of economic and financial development in Asia and elsewhere and his books include “Asian Stock Markets – the Inside Story” published by Dow Jones Irwin in 1986 as well as “The Barons of European Industry” published by Croom Helm in 1973.