Time to Prick the Dollar Balloon, Gently

Time to Prick the Dollar Balloon, Gently

MEDFORD, MASS: The United States has a large, growing, and ultimately unsustainable current account deficit. Experts disagree on how long the trends can continue: Will the patterns reverse on their own, or will massive policy changes be needed to prevent widespread and "disorderly" adjustments? Hilton Root argued persuasively in a recent YaleGlobal column that the current US account deficit was less of a problem than some observers suggested. Not all, however, are persuaded.

One way to assess the threat of the ballooning US debt is to understand the perspective of the Asian central banks, who have recently become the "buyers of last resort" for US Treasury Bills. How long will they continue to support US debt? There is a compelling argument to slow the binge. Indeed, the central banks refrained from bidding in the September Treasuries auction. If they decide to abstain from buying into US debt for the time being, the landscape for the dollar will certainly change.

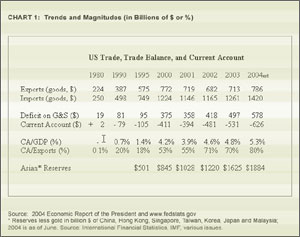

The US current account deficit – the shortfall between the country's export and import – has been growing for some time. From 1995 to 2004, while imports grew 90 percent, exports of goods grew only 37 percent; in the same period, the current account deficit increased by over US$500 billion. Over half of the accumulated US deficits since 2000 have been absorbed by the Asian nations. [See table]. These Asian reserves comprise 120 percent of the value of those nations' annual imports – far more than needed for emergency expenditure, even allowing for interest payments on debt.

Assuming that US exports were to keep pace with world trade, and imports continued to amount to about 15 percent of nominal GDP growth, US imports will grow by approximately US$100 billion a year; export growth, however, would be a fraction of that total. One recent paper by Nouriel Roubini and Brad Setser reported, "If current trends continue, Asian central bank reserves would have to rise from an estimated US$2.4 trillion at the end of 2004 to US$4.3 trillion at the end of 2008 to help support a rise in US net external debt from US$3.3 trillion to US$6.9 trillion."

However, the report warned, as US deficits rise, private investors will likely pull back from buying into US debt – forcing the Fed to intervene massively to shore up the dollar. In a recent Economist special article, Fred Bergsten cited a projection of the current account deficit of 10 percent of GDP in 3 to 4 years – that would be US$1.5 trillion per year in financing needs! Amounts of this magnitude would be impossible to finance.

An Asian central bank manages currency for an economy that often has more dollars coming in than it has going out. The central bank usually maintains a large US dollar reserve and then buys Treasuries. This keeps its exchange rate steady against the dollar (or nearly so) but pumps local currency into the economy. The rise in money and credit can spark a boom – whether in real estate, investment, or even consumer spending – that can eventually lead to bad loans and bank problems. Imbalances build up, and the economy becomes overheated.

What if the central bank did not buy the Treasuries? Then the local money supply would be lower, and the value of local currency would increase relative to the dollar. This might not be so bad if it only involved a single country and the United States. However, China, Malaysia, and Hong Kong keep their currencies officially pegged to the dollar. The country that stops buying dollars will see the price of its exports rise relative to countries like China. In fact, several other nations monitor the Chinese currency so that their products do not become more expensive in relation to China's. Thus, there is a coordination problem: All will benefit only if all, or nearly all, act together.

What are the benefits of not buying Treasuries? The first is that imports become cheaper in local currencies. This allows more investment (cheaper capital goods), faster growth, and higher quality of life. Secondly, there is less overheating and bubbles, as discussed above. The third benefit is that the central bank is not left holding dollar-based assets, which, after certain depreciation, would prove a bad investment.

Most economists would object, claiming that the goals of a central bank are to control inflation and promote stable growth, not to make a killing or avoid losses in Treasury securities. Exactly. By recognizing the inevitable and avoiding excessive and unproductive intervention in the foreign exchange markets to support the dollar, inflation and instability are reduced and losing investments are avoided.

The solution is obvious, but difficult. The major official buyers of US Treasuries would have to act together to reduce purchases. They should allow their currencies to float or move in controlled steps upwards against the dollar, but not against each other. The point of this exercise is not to "punish" the US, but to give it market information that is now obscured by the peculiar institutional structure. With this solution, the dollar's loss of value will underscore the urgency of curbing US budget deficits, boosting private savings and energy efficiency, and favoring local production over imports. Forcing an earlier adjustment would minimize "disorder" in both US and global markets.

Even so, the adjustment might not be smooth. On the US side, with decreased foreign demand for dollars, the interest rate would be hiked up to make the Treasuries attractive. If the optimists are correct, and private investors are just waiting for the dollar to fall to come back in and buy US assets, then a smaller dollar decline would be needed – and the sustainable current account deficit might be higher than the pessimists now assume. Even so, a hike in interest rates would depress housing and stock prices, causing consumer retrenchment and perhaps a US recession. If the pessimists are right, the decline in the dollar would go further and the dislocation would be greater. To avoid this, central banks might want to fight speculation that led to really excessive declines in the dollar.

If the current situation continues, with foreigners accumulating over US$6 trillion in Treasury assets, then the dollar must decline relative to most other currencies. Thus, Treasuries-holding nations would lose more than US$2 trillion in purchasing power. This considerable cost is enough to make it an urgent priority rather than a "back burner" issue. Neither presidential candidate has a credible proposal to reduce the US deficit by much. This suggests that US savings will remain low, and foreign borrowing will remain high, until the cost becomes unacceptable. The creditors must act as if they have an interest in rational debtor behavior. If they do not, the costs all around will be higher than anyone wants to imagine.

David Dapice is Associate Professor of Economics at Tufts University and the economist of the Vietnam Program at Harvard University’s Kennedy School of Government.