US Recession: Spend Now, Save Later

US Recession: Spend Now, Save Later

SINGAPORE: The governments want their citizens to go shopping and reverse the economy’s slide toward recession. But consumers, as the Bush administration found out, cling to their tax rebates and avoid the shopping malls.

Now the Obama administration gears up to provide massive stimulus to create jobs and get people spending again. The fate of the US economy and that of the world hangs on the success of his effort. If history is any guide and people behave the way one school of economic thought predicts, the chances do not appear bright. Unless citizens are convinced that their future earning will be more than the total of their annualized income from job or business, they are more likely to save than spend. The health of the world economy depends on US performance, which in recent years emerged as the principal engine of growth. In 2007 , private consumption reached 71 percent of the US gross domestic product, after standing steady at about 62 percent for more than 30 years, from 1950 to the early 1980s. American consumers turned their economy into an engine of growth at the expense of economic balance, as consumption far outran production, resulting in a debt race never seen before in peacetime.

Understanding how such a rapid change occurred is critical to understanding consumer behavior during this crisis. A clue is found in comparing asset prices with consumption as share of GDP. Stock-market prices were also basically stable from 1950 to the mid-1980s, moving slowly upwards during the second half of the 1980s to take a mighty jump from the early 1990s to 2008, with a brief interruption when the IT-bubble burst in 2000. Housing prices, adjusted for inflation, were basically unchanged from 1950 to 2000, thereafter expanding into the property bubble that started to burst in 2006. Exactly at the moment when share prices leveled off, their stimulatory impact was replaced by property prices; when both stopped going up, consumption was hit, no longer stimulating the economy but pushing it into contraction.

The theory about consumption coined by economist Franco Modigliani about 50 years ago reveals the effect of asset prices on consumption and offers insights for judging how effective proposed US expansionary measures might be. Broadly speaking, the theory suggests that expectations and stability are crucial, that people consume portions of their anticipated lifetime income steadily throughout their lives. Lifetime horizon means that temporary fluctuations in income do not influence consumption. Instead the consumer absorbs fluctuations by building up or running down wealth: Young people borrow, anticipating higher incomes, the middle-aged save more and the elderly exhaust their savings.

This is precisely what happened in the US during the last decade. With property prices soaring, individuals changed their perception of resource availability over the course of their lifespan. Expecting constantly growing resources in terms of asset price, consumers spent more money. When asset prices suddenly turned around, falling instead of rising, the individual was caught flatfooted, forced to reduce consumption and increase savings, reestablishing the consumption equation steered by lifetime income only: Despite any federal government splash-out of funds, consumers cannot be expected to return to past behavior as happy spenders.

When the Great Depression started with the stock-market crash in 1929, conventional economic wisdom was to lower interest rates, making it more profitable to invest and triggering higher investment, thus stopping the economic downward spiral. Yet, that did not happen. Companies did not invest even if the money was almost free; instead, they hoarded cash. British economist John Maynard Keynes saw that monetary policy, with lower interest rates, would not work, because of the liquidity trap: Faltering demand discouraged investment even when debt carried little cost. Consequently, he ordained demand stimulus via fiscal policy, even if contrary to conventional wisdom, it meant rising public deficits and higher public debt. The policy worked.

Now we’re in a congruous position with regard to fiscal stimulus. With the lifetime consumption theory in mind, it’s unlikely that money handed out will be spent. So we move into what Keynes might have labeled a “fiscal policy trap,” meaning that regardless of money poured into the economy, spending will not go up. Spending will rise only when the individual concludes that future resources warrant increased spending. The brutal fact is that the US cannot spend its way out of the crisis. On the contrary, the more the US spends, the more likely individuals will deduct limits to future resources, because debt incurred must be repaid, meaning future higher taxes and less disposable income. This may well prove to be the revelation to the science of economics of the present crisis.

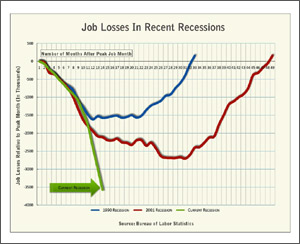

People may ask why fiscal stimulus helped in the 1930s, but is judged to be impotent now. The answer is, in 1929 when the Great Depression struck, the US debt level was far lower than today’s level. Broadly speaking, total debt amounts to almost 400 percent of GDP in 2009, compared with 170 percent in 1929.

Pump-priming, as proposed by government stimulus plans, will be hoarded by consumers to reduce their debt as money was hoarded in the 1930s. There’s a clear parallel to Japanese companies in the 1990s, which used capital to rebuild balance sheets, not to invest. The lesson is clear: It’s no use giving people money to spend if economic rationale tells them to save. The most noteworthy aspect of pump-priming will be redistributing savings between the private and the public sector with no visible effect on production, consumption and employment.

So what can be done to extricate the US from “the fiscal policy trap”?

Consumption patterns cannot be rolled back to boost the economy. Demographics works against higher consumption with the increase of households primarily taking place in the age bracket 50 years and older, with its low propensity to consume. What’s needed is a restructuring of the US GDP – acquiescing to a lower share for consumption and welcoming a higher share for investment and net exports compared to the last decade or two. This calls for an orchestrated panoply of policy measures that require years to work through the system. Understandably, the loss of jobs calls for action. The American export engine is unlikely to be fired up again. But a combination of measures to enhance the skill of the workforce, allowing the US to regain some of its competitiveness, and extended unemployment benefits as a temporary help until the economy grows again might prove effective and at the same time address fundamental problems behind the present calamities, including loss of competitiveness plus economic and social inequality.

The best way is to take the bull by the horns and stimulate savings to eliminate the oppressive debt burden, thus restoring balance between production and consumption and lay the foundation for future growth. The contraction or lower growth imposed by debt-reducing policies may be worth sustaining. The alternative now pursued, including massive tax cuts, is running up an even higher debt, jeopardizing confidence in re-balancing the economy and undermining long-term capability to restore sustainable growth spearheaded by investment and net exports.

A quick fix cannot redress a fundamental disequilibrium. The more frenetic attempts to deliver a policy solution here and now will most likely not address the fundamental disequilibrium underpinning the crisis. The stimulus should be for saving and enhanced competitiveness rather than spending.

Joergen Oerstroem Moeller is a visiting senior research fellow with the Institute of Southeast Asian Studies, Singapore, and adjunct professor at Copenhagen Business School & Singapore Management University.