Global Currency Accord Is Necessary, But Unlikely

Global Currency Accord Is Necessary, But Unlikely

JAKARTA: Major economies should pursue currency agreements to stabilize the US dollar, especially during the COVID-19 crisis, preventing a rapid rise against other currencies that is sure to trigger calls for protectionist measures.

There is historical precedent. In 1985, the US dollar soared. The United States, West Germany, Japan, France and the United Kingdom – the Group of 5 world powers – met at the Plaza Hotel in New York on a Sunday in September, when markets were closed. Four nations agreed to appreciate their currencies to depreciate the US dollar.

Multilateralism and discrete action were necessary to realign exchange rate stability and counter the strong dollar in the early 1980s, with particular significance to West Germany and Japan, two former adversaries that were gobbling up increased US industrial output.

Former US Treasury Secretary James Baker III convened the meeting, expressing concern about rising protectionist sentiment among US industrial interests over an account deficit for the United States and surpluses posted by Japan and Germany. The meeting, held in stealth, was based on Baker’s close relationship with then President Ronald Reagan, whose trust he had gained earlier as chief-of-staff. Baker’s idea ran counter to Reagan’s policy about controlling inflation with a strong dollar, but the president listened and liked the idea, knowing that protectionism over the long haul would do more to damage markets than promote domestic interests.

The global economy faces a more calamitous situation today, namely with the COVID-19 pandemic, which has destabilized world markets and caused the dollar to rally against other world major currencies in a few weeks. Countries have feasted on cheaper, liquid dollars for several years and now the piper calls.

In essence, a new Plaza Accord is necessary, even more so than in 1985, to soothe market volatility. Nonetheless, consider the many monetary changes over the last 35 years that may preclude such action:

● World capital markets are much deeper, more complex and electronically integrated than in 1985.

● Unilateralism, not multilateralism, is the guiding theme that most countries now pursue, as led by the United States.

● China, a dollar-backed economy, would not readily agree to depreciation of its vast dollar holdings.

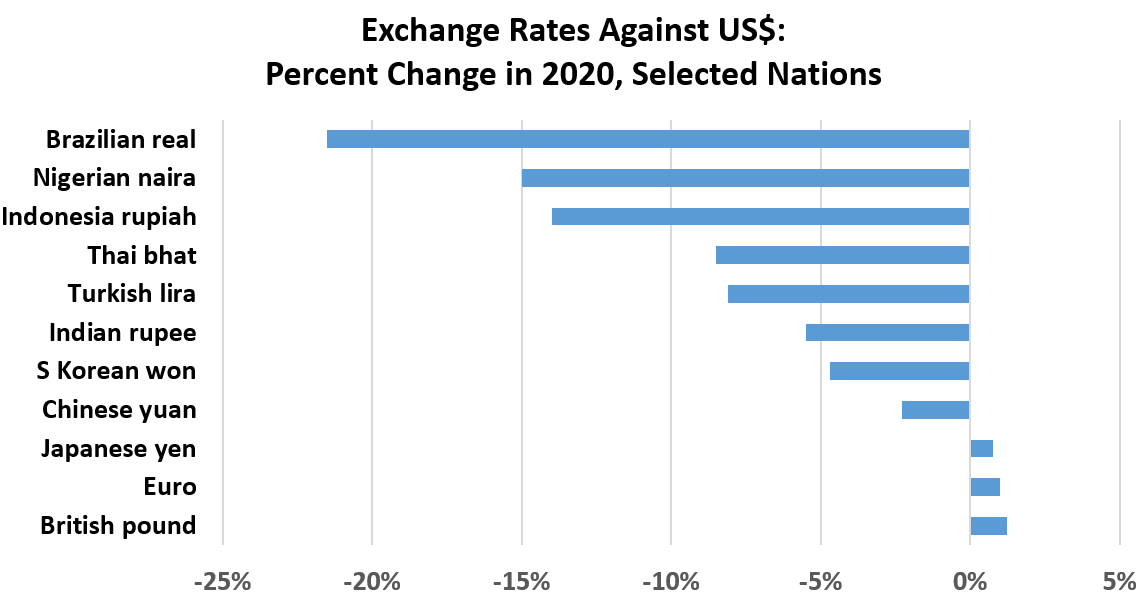

First, regarding the capital markets, dollar credit accounts for 14 percent of all non-bank global GDP as of 2018. In fact there are more $100 bills circulating worldwide than $1 bills, with 80 percent outside the United States. Bonds, loans and payments around the world are today denominated in dollars. These are not dollars owed to the United States, but rather covenants made between various parties that rely on the dollar as the most stable currency and the only game in town. The financial calamity caused by the coronavirus has delayed payments in king dollar, with numerous defaults expected soon or debts called in by creditors early. This has precipitated a global ripple. Dollars must be had, and quickly, or depreciating local currencies will result. The crisis has not spared even so-called safe-haven currencies such as the Japanese yen and Swiss franc from volatility, due to their liquidity for such payments. During crises, lenders seek to minimize risk. Further, commodity currencies, such as the Norwegian krone and Canadian dollar, which garner most of their support from stable oil prices, quickly depreciated with Saudi Arabia and Russia warring over oil-production cuts in the face of slackening demand.

Second, with unilateralism, protectionism ensues. Countries try to contain the carnage on their own. Coordinated leadership is required. The US president, strongly unilateralist, seeks to influence economic policy directly. In the process, he has undermined trust among nation-states that he perceives as abusing US markets. This contrasts with Reagan’s style in 1985, authorizing Baker to pursue multilateral negotiations on his own. Massive credit “swap” lines, contracts recently opened by the US Treasury to reduce risks and assist aligned countries with dollar loans, are not enough to stem the tidal wave of demand. There are simply not enough dollars in the system to placate all outstanding dollar indebtedness. These debts include dollar-denominated sovereign and corporate issues from countries like Indonesia or Nigeria, which were later sold on world markets. Such bonds were not only absorbed by US investors, but also by those in the United Kingdom, Singapore, Dubai and China.

Third, China holds more foreign exchange reserves than any other country in the world, at last count, around $3 trillion. Foreign exchange is synonymous with the US dollar, generally speaking, with 62 percent of world reserves in dollars and euros a distant second at 20 percent. It would work against Chinese interests to devalue the yuan further. China, not a party to the 1985 Plaza Accord, is today the second largest economy in the world, and its vast dollar reserves have assisted the nation in weathering financial storms better than other countries. Much of this was born during the financial crisis in 1997, when most Asian countries lacked the dollar reserves necessary to placate the stampede on local currencies.

Yet such an agreement is unlikely.

This time, developing countries are loaded for bear, hoarding dollars to the extreme. Nonetheless, many developing countries, such as Nigeria, Lebanon and Turkey, have a much larger dollar debt-to-reserve ratio, even with large holdings, and feel the dollar squeeze.

Nothing would assuage world markets more than orderly depreciation of the US dollar, with stabilization and appreciation of other currencies. A multilateral approach – conducted by a handful of leading finance ministers, with the backing of strong US financial leadership, away from news media – might calm global markets. None would want to tip the markets early, similar to the 1985 agreement when orderly depreciation of the dollar occurred and accomplished the immediate goal of rebalancing the dollar.

Today, the G20 has many more actors, many with political tendencies that resist the appearances of compromise. The European Union’s euro, successor to the French franc and deutsche mark, did not exist in 1985. Further, the digital world instantaneously conveys currency moves of any type. Any sudden market move would invite not only speculators, but also reactionary capital controls from governments, both on dollar holdings and domestic currency. Nonetheless, this trying time of pandemic and collapsed oil prices mandates compromise and multilateral action – along with cooperation from a US president who holds his position based on "America first" policies.

To be precise, the Plaza Accords were a prescription to soothe a short-term symptom of uncontrolled dollar strength, exactly what the world experiences now. Soon afterward, another agreement, the 1987 Louvre Accord in Paris, halted the dollar’s 18-month decline, exacerbated by speculators. Once again, the G5 agreed to exchange their currencies in a range, with a compromise between a pure floating and fixed-exchange rate system. Japan was recognized as a world financial powerhouse during the Plaza Accord, and swelling of the yen’s value from ¥250 to ¥150 per dollar in a few months contributed to asset bubbles and fiscal mismanagement, eventually leading to stagnant growth and the “lost decade” of the 1990s for the Japanese economy. Nevertheless, the real target of both accords was West Germany, with its growing industrial might threatening to overwhelm US industry with an artificially low deutsch-mark exchange rate.

Left unchecked, a soaring dollar will wreak havoc in emerging markets with rising inflation, collapsing currencies and a decline in US competitiveness. The 1985 agreement may have marked the last great initiative for multilateral control of the dollar’s ascendancy.

Will Hickey is a former Fulbright scholar and visiting professor with Guangdong University of Foreign Studies, Canton, China. He is also author of The Sovereignty Game: Neo-Colonialism and the Westphalian System, 2020, and Energy and Human Resource Development in Developing Countries: Towards Effective Localization, 2017.

Comments

I'm glad I am no longer paid in Indonesian Rupiah !